The Schindler Group from Central Switzerland reports unusual ups and downs on its segments. But this is not the only thing that is strange.

Anyone leafing through the semi-annual and annual financial statements of the family-owned company, which specializes in escalators and elevators, will quickly rub their eyes.

Their segment reporting is quite unusual.

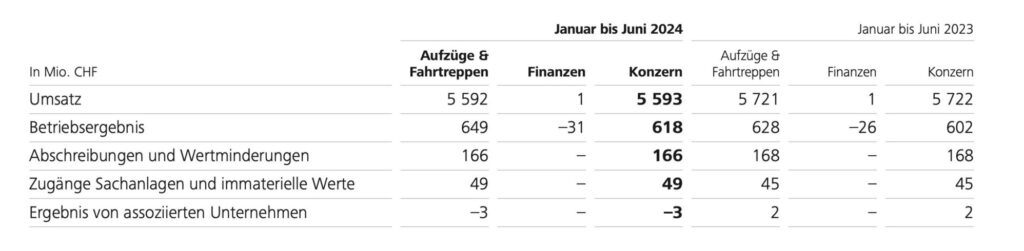

Only one million in sales

The Schindler Group recently announced that it had achieved sales of around 5.6 billion Swiss francs and an operating profit of around 650 million Swiss francs in the “Elevators and Escalators” segment in the first half of the year.

In the second segment, called “Finance”, however, sales in the first half of the year amounted to only one million Swiss francs, resulting in an operating loss of 31 million Swiss francs.

The “Finance” segment includes the expenses of Schindler Holding AG and the business activities of BuildingMinds, the Group explained.

Huge difference

Companies normally provide insights into sub-segments of their activities in segment reports.

However, in the case of the Schindler Group, virtually the entire turnover is generated in one division.

If you also look at the annual financial statements, the company only ever shows the two segments “Elevators and Escalators” and “Finance”.

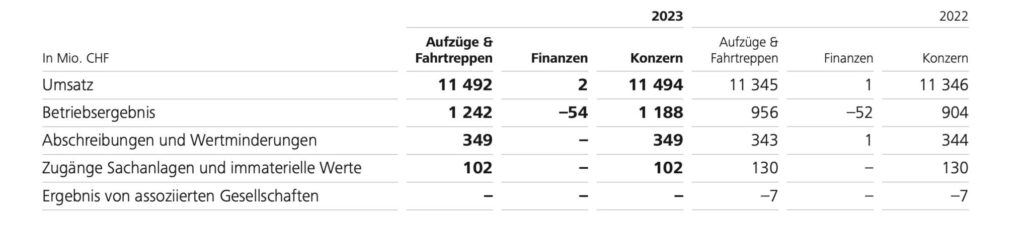

In 2023, the larger segment generated revenue of around 11.5 billion Swiss francs and the other segment only 2 million Swiss francs.

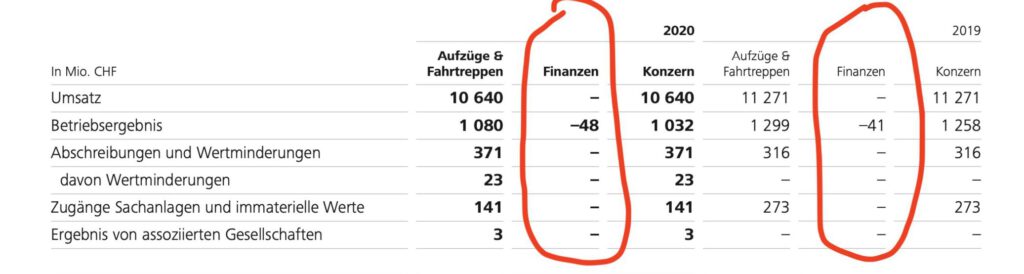

In 2019, for example, there was no turnover at all in “Finance”.

Clear rules according to IFRS

According to its own advertising, the Schindler Group has developed into “one of the leading providers in the elevator and escalator industry” over the past 150 years.

Shouldn’t the company at least tell investors how much turnover and operating profit it generates in both areas?

Schindler’s segment reporting follows the International Financial Reporting Standards (IFRS) and is therefore based upon the company’s own internal financial reporting.

Both the definition of the segments and the segment information to be published are therefore based on the data used for internal performance measurement and resource allocation.

The fact that the holding company at Schindler is practically only there for financial purposes also seems somewhat strange for a company led by CEO and Chairman of the Board of Directors Silvio Napoli.

According to the IFRS textbook, websites written in a different language define an operating segment as:

“A component of an entity that a) engages in business activities from which it earns revenues and incurs expenses, b) whose operating results are reviewed regularly by the chief operating decision maker to make decisions about resources to be allocated to the segment and assess its performance, and c) for which discrete financial information is available”.

Points a), b) and c) should therefore certainly apply to Schindler’s escalators and elevators.

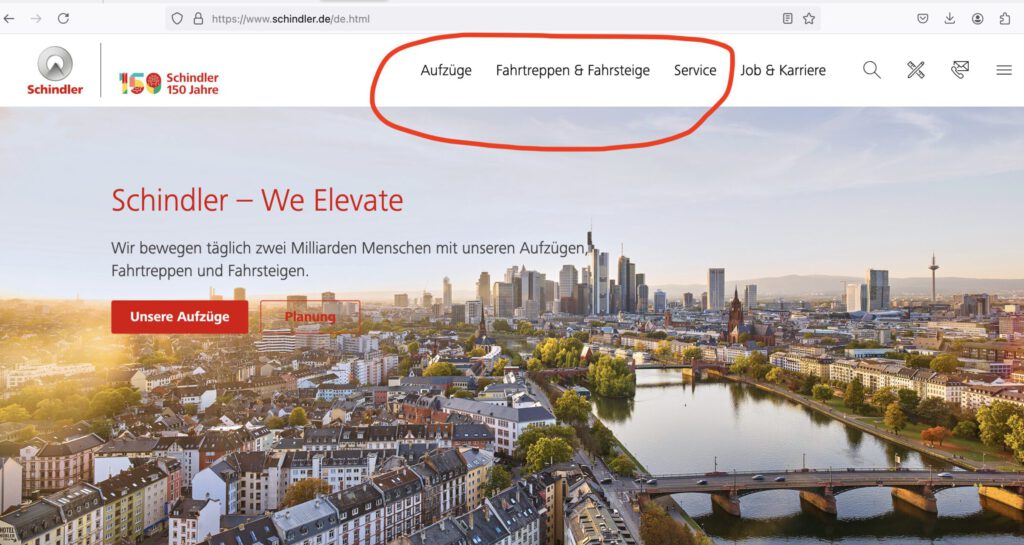

If you look at the websites of individual Schindler national companies, you will also find the division into escalators and elevators.

In Germany, for example, the Schindler website is clearly divided into Elevators, Escalators & Moving Walks and Service. (see screenshot).

Internally with additional information

“The Elevators & Escalators segment is managed as a global unit and comprises an integrated business that includes the production and assembly of new installations as well as the modernization, maintenance and repair of existing installations,” Schindler states regarding that segmentation.

However, it is immediately stated that internal financial reports are made available to the Supervisory and Strategy Committee as the main decision-makers and that these reports form the basis for the assessment of the segment’s performance.

The management therefore apparently has more information.

Silence in the forest

muula.ch then wanted to know from the Schindler Group’s media office why the segment reporting was not broken down further.

However, an overwhelmed media spokeswoman simply replied with the same references to the interim and annual reports that muula.ch had given her the day before to help her understand the media inquiry.

Inquiries to the head of communications and even to the main person responsible, Napoli – about this actually harmless question – has since remained unanswered.

This is usually a bad sign for any listed company, as journalists then know that they have probably hit upon a sore spot.

The company’s behavior is therefore strange.

Auditors give their blessing

muula.ch, however, went on to ask several accounting experts about the Schindler Group’s segment reporting.

They were unanimous in their opinion that it was rather strange with the rough split.

The accounting specialists were also surprised that the auditors at PwC and Ernst & Young have both accepted this questionable presentation for years.

Legally, this approach was ‘probably okay’ they said.

External parties in the dark

Furthermore, the Schindler Group could not even get out of the affair with the argument that it did not want to give its competitors Thyssen, Otis, Kone & Co. any insight into the profit margins of elevators and, separately, escalators.

According to IFRS, there are no clauses to protect against competitive disadvantages resulting from the disclosures, as clearly stated in the rules governing the business segments.

Board of Directors buys shares

At the end of July, a member of the elevator and escalator manufacturer’s Board of Directors made a large-scale purchase of Schindler shares.

According to a disclosure report to the Swiss stock exchange SIX, this director acquired 605,140 registered shares with a total value of 133.1 million Swiss francs.

However, if the Board of Directors is better informed about the business situation and profitability of elevators and escalators, then this share deal would probably also leave a greasy aftertaste.

Providing a target

“We have learned from this and drastically improved our crisis management,” CEO and Chairman Napoli recently told the “Neue Zürcher Zeitung” newspaper about a death involving a boy in Japan, in which the entire public opinion turned against the lift manufacturer.

‘You are always wiser afterwards’ emphasized the company boss regarding one of the family company’s biggest crises.

However, there is obviously still room for improvement in crisis management – because companies are often attacked by short sellers, for example, precisely because of questionable accounting methods.

05.08.2024/kut./ena.