The Swiss franc’s status as a ‘safe haven’ is bringing Switzerland cash. However, this leaves the National Bank with only one option for action.

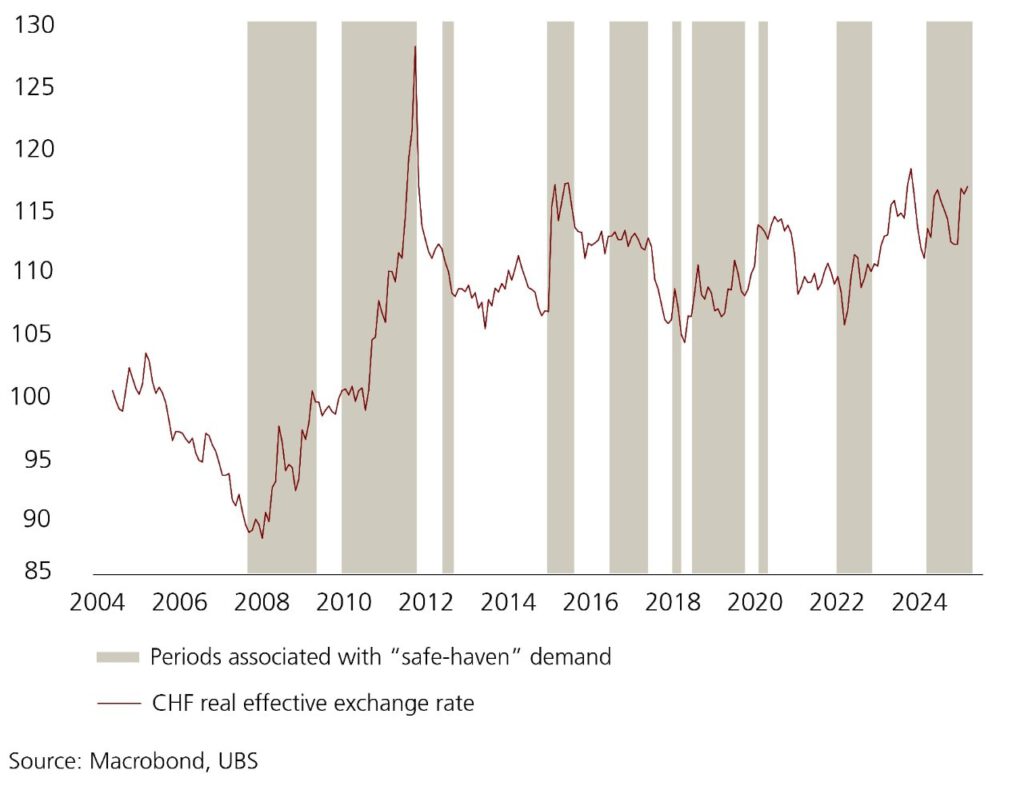

The good news is that the Swiss franc is likely to remain attractive as a safe-haven currency.

In times of global uncertainty and geopolitical tensions, people seek stable investments, and this includes the Swiss currency.

Already appreciated by 10 percent

However, in times of increased risk aversion, global currency preferences also lead to corresponding side effects, which are now becoming even more apparent for the Swiss franc and are undermining the competitiveness of the economy in addition to those US punitive tariffs.

Since the beginning of the year, the Swiss franc has appreciated by 10 percent against the dollar.

The franc’s ‘safe haven’ status ensures low interest rates and saves households and companies around 28 billion Swiss francs per year, according to calculations by the major Swiss bank UBS, as the financial institution calculated in its latest economic outlook this week.

On top of that, the public sector saves around 5 billion Swiss francs per year in interest payments, it added.

That adds up to 33 billion Swiss francs in annual benefits.

Investors are willing to pay a premium for safe, liquid assets, and the attractiveness of the Swiss franc as a safe-haven currency lowers interest rates in Switzerland by an estimated 2 percentage points.

Many positive effects

A strong Swiss franc benefits the country’s consumers by making imported goods and services more affordable.

Since 2009, these savings have amounted to an average of around 0.3 percent of private consumption per quarter, or 1.2 billion Swiss francs, according to UBS economists.

A strong Swiss franc makes imports cheaper and also lowers consumer prices. With low inflation, wage increases do not need to be as high, which in turn saves money for the state coffers and companies.

And even the chosen definition of inflation in Switzerland contributes to low inflation being reported, as muula.ch recently revealed.

Cheaper imported inputs

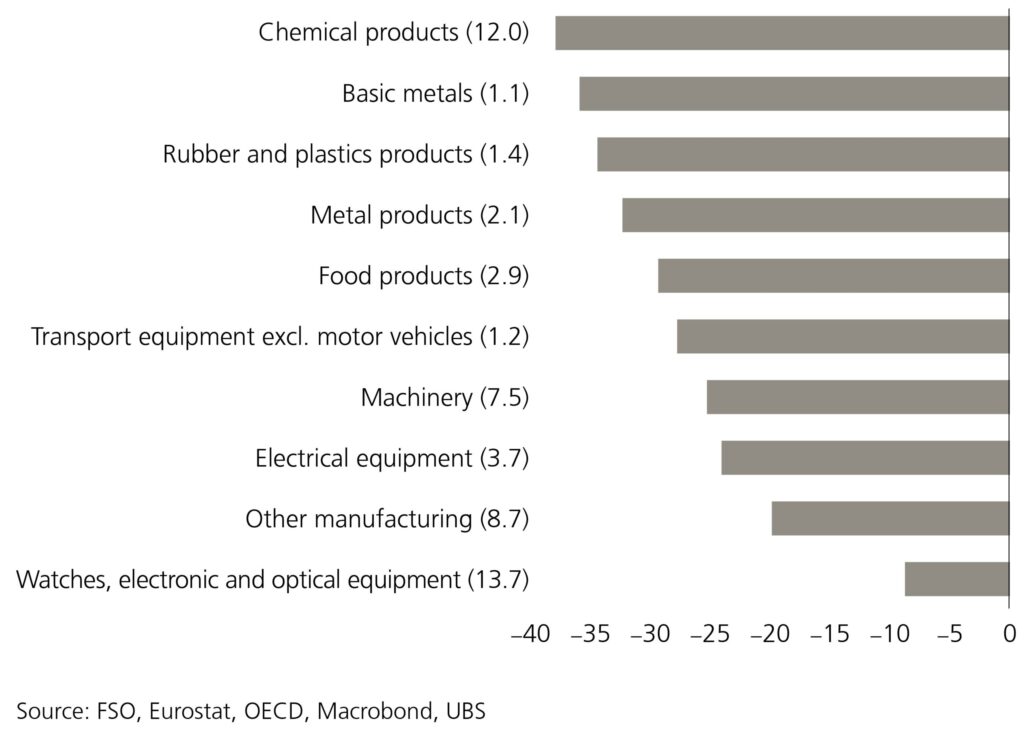

What applies to consumers also benefits companies, of course.

A stronger Swiss franc lowers the cost of imported inputs, as Swiss exporters import around 30 percent of their inputs.

According to UBS, Swiss companies pay 20 to 40 percent less for their imported intermediate goods than their German competitors compared to 2009, with the exception of watches and precision instruments.

Competitiveness therefore results solely from such effects. However, this does not have a complete impact.

Depending on the sector, imported intermediate goods account for only 20 to 35 percent of the export value, meaning that these savings only partially offset the negative impact of the franc’s appreciation on exporters’ margins.

Additional pressure to act

However, this complex situation means that there is little scope for further interest rate cuts in monetary policy, and savers have to accept low returns.

The Swiss National Bank (SNB) is thus facing a monetary policy dilemma: interest rates are around 2 percentage points lower than they would be without the ‘safe haven’ effect.

If global confidence in the dollar continues to wane, the Swiss franc could appreciate even further, which would put additional pressure on the SNB to act, according to UBS.

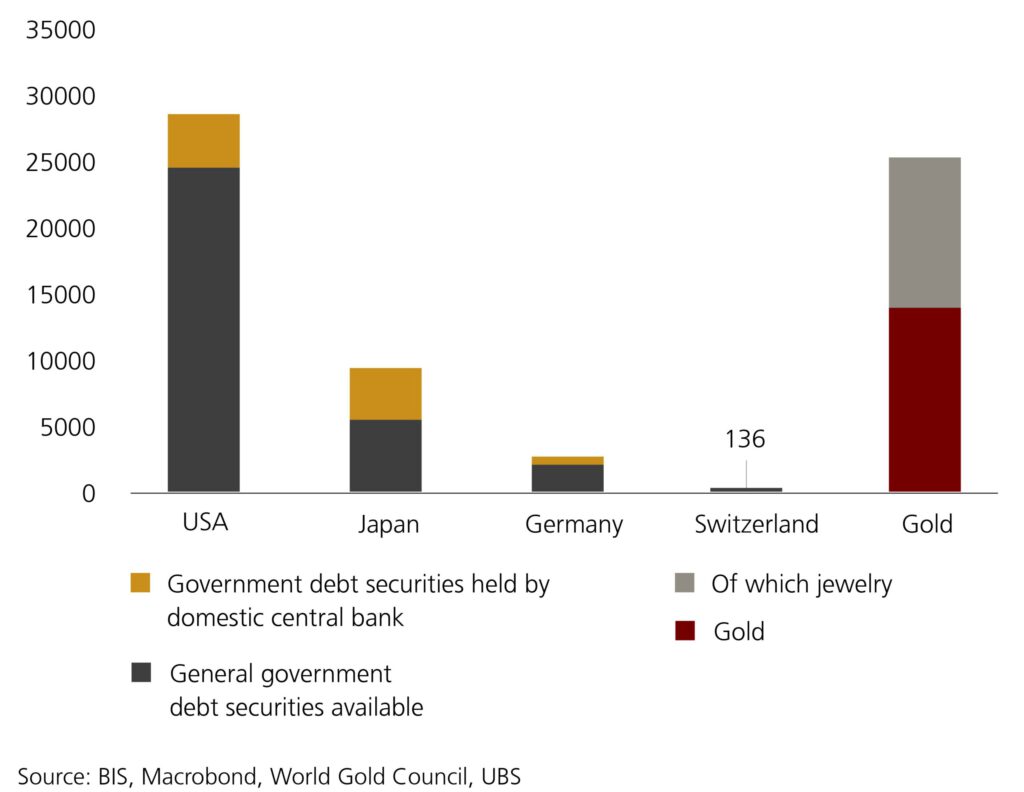

Swiss market too small

However, the limited availability of highly liquid and secure assets in Swiss francs is putting considerable upward pressure on the currency.

This is similar to the upward pressure seen on the gold market since 2022, it added.

This leaves the SNB with only one option: to intervene in the foreign exchange market and weaken the Swiss franc there. To do so, however, the SNB must print money and buy dollar assets.

This is considered to be currency manipulation, and the dollar purchases could become less and less valuable over the long term, meaning that the SNB is knowingly entering into such loss-making transactions.

12/09/2025/kut./ena.