The turmoil in the energy market has caught state-owned Axpo cold. But the catastrophe only shows up deep in their annual report.

The whole sentences sound so passive – as if the energy group Axpo is not an active player in the market. “The past financial year was characterized by unprecedented distortions on the energy markets and market price developments had a very different impact on results, balance sheet items and cash flows in the 2021/22 financial year.”

With these words, Switzerland’s most important energy group commented Thursday on its results for the fiscal year ended September.

Shock in the fine print

But what is meant by all of this is not so apparent at first glance. Profit and equity were virtually unchanged from the previous fiscal year at 600 million Swiss francs and around 7.4 billion Swiss francs, respectively.

But looking deeper by muula.ch into Axpo’s annual financial statements shows us that sales increased by over 70 percent to 9.9 billion Swiss francs. On the other hand, costs for energy procurement and grid usage expenses rose by around 160 percent to 9.6 billion Swiss francs.

Into the shark tank

It turns out that the markets can also go in the other, less favorable direction, and if Axpo wants to swim with the sharks, this state-owned company must have the right tools to do so.

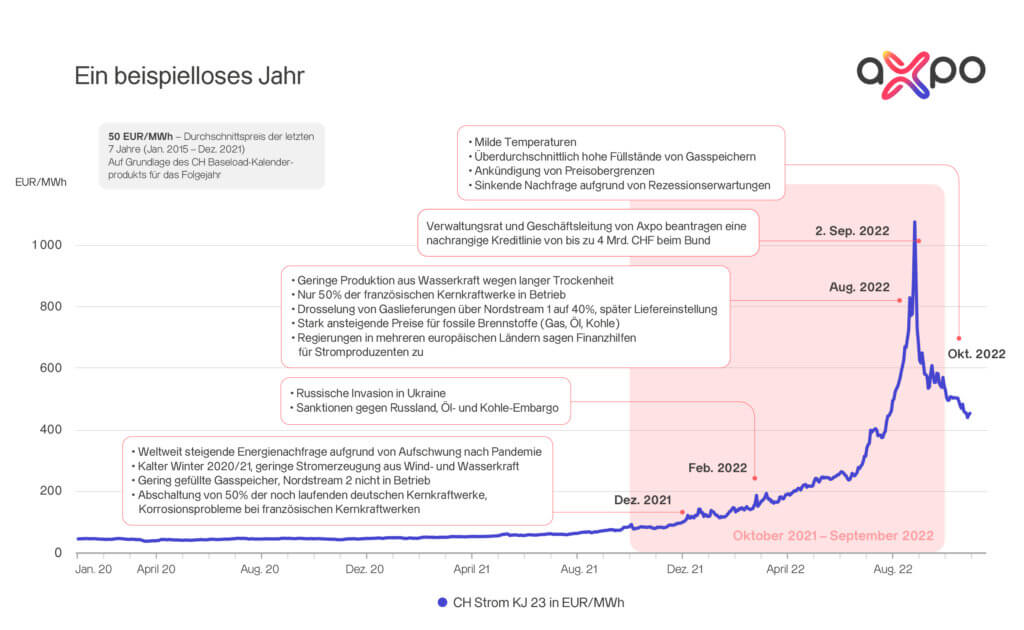

After all, it is unlikely, but not impossible, that the wholesale prices of electricity and gas are at times 20 times higher than the average of recent years.

Billions up

As a result, the value of long-term derivative financial instruments on Axpo’s assets side increased by 10.5 billion Swiss francs, or around 160 percent, to 17 billion Swiss francs.

Short-term financial instruments amounted to an additional 18 billion Swiss francs – an increase of almost 100 percent or a further 10 billion Swiss francs.

Energy markets are going crazy and Switzerland’s Axpo is in the middle of it. (Image: media service)

On the liabilities side, however, short-term derivative financial instruments soared by 220 percent, or 16.2 billion Swiss francs, to 23.5 billion Swiss francs.

Long-term financial instruments added another 24.8 billion Swiss francs – an increase of around 10 billion Swiss francs or 70 percent.

Gigantic net debt

With all this, total assets increased by around 80 percent to almost 80 billion Swiss francs. This is equivalent to around 10 percent of Switzerland’s gross domestic product (GDP). You have to imagine that for a single company.

Axpo’s equity ratio shrank from 16.2 to a mere 9.3 percent as a result of the balance sheet expansion.

The balance sheet expansion was a result of accounting rules that assign a replacement value dependent on the market price to contracts for energy deliveries and the corresponding hedging transactions in the future.

Net debt increased in this context from 223 million Swiss francs to 3.6 billion Swiss francs.

Special effects had an impact of 1.4 billion Swiss francs on the operating result, the new annual report stated succinctly. In the previous year Axpo had recorded only minus 127 million Swiss francs in this area.

Sausage hangs in the future

The return on the decommissioning and disposal fund in 2021/22 was namely minus 13.6 percent (previous year: +12.4 percent), burdening the operating result at EBIT level by 327 million Swiss francs and the financial result additionally by 410 million Swiss francs.

Due to the lack of liquidity in the Swiss market, the majority of Swiss production is hedged in Germany and France. Price differences between Switzerland and Germany increased many times over in the past fiscal year.

This led to shifts in earnings to subsequent years due to the accounting treatment of the financial instruments used for hedging amounting to 1.5 billion Swiss francs alone. The risks are borne by the owners – i.e. the people.

Axpo appreciates assets

But things didn’t just go in the negative direction for the Axpo Group. Due to rising electricity prices, “the value of the company’s own power plants had to be reviewed,” it said soberly.

Since electricity prices rose sharply not only in the short term, but also in the medium term, a write-up of no less than 3,150,000,000 Swiss francs was recorded in the past 2021/22 financial year.

Axpo thus generated a profit of 3.2 billion Swiss francs on its own assets. If energy prices go in the other direction again, everyone can figure out what is threatening in this position. The speculations of the company in public hands continue.

Currency risks involved

The electricity generated by the Axpo Group in its Swiss power plant park needs an immediate buyer. Trading is therefore inextricably linked to electricity production, the energy group stressed again on Thursday.

Electricity produced in Switzerland by Axpo is delivered when there is demand in Switzerland, even if the hedging happens on international markets. This shows that Axpo not only engages in energy speculation, but even accepts high currency risks via the Swiss franc.

Hedging sounds cute, but it’s not risk-free.

Expensive experience

Cash flow from operating activities decreased from 888 million Swiss francs in the previous year to minus 3.1 billion Swiss francs, mainly due to the deposit of additional collateral precisely for the hedges of Swiss electricity production.

“Our company will continue to develop as a result of these experiences and will emerge from the crisis stronger,” Axpo Group CEO Christoph Brand was quoted as saying in a communiqué regarding their annual financial statements.

Let’s hope that the shock at Axpo is deep enough and that the state-owned group takes the right measures to reduce energy speculation.

08.12.2022/kut./ena.